.webp)

Student debt is a major financial headwind for many American households, and the rules of the game are changing in ways that will shift the budget math around student loans.

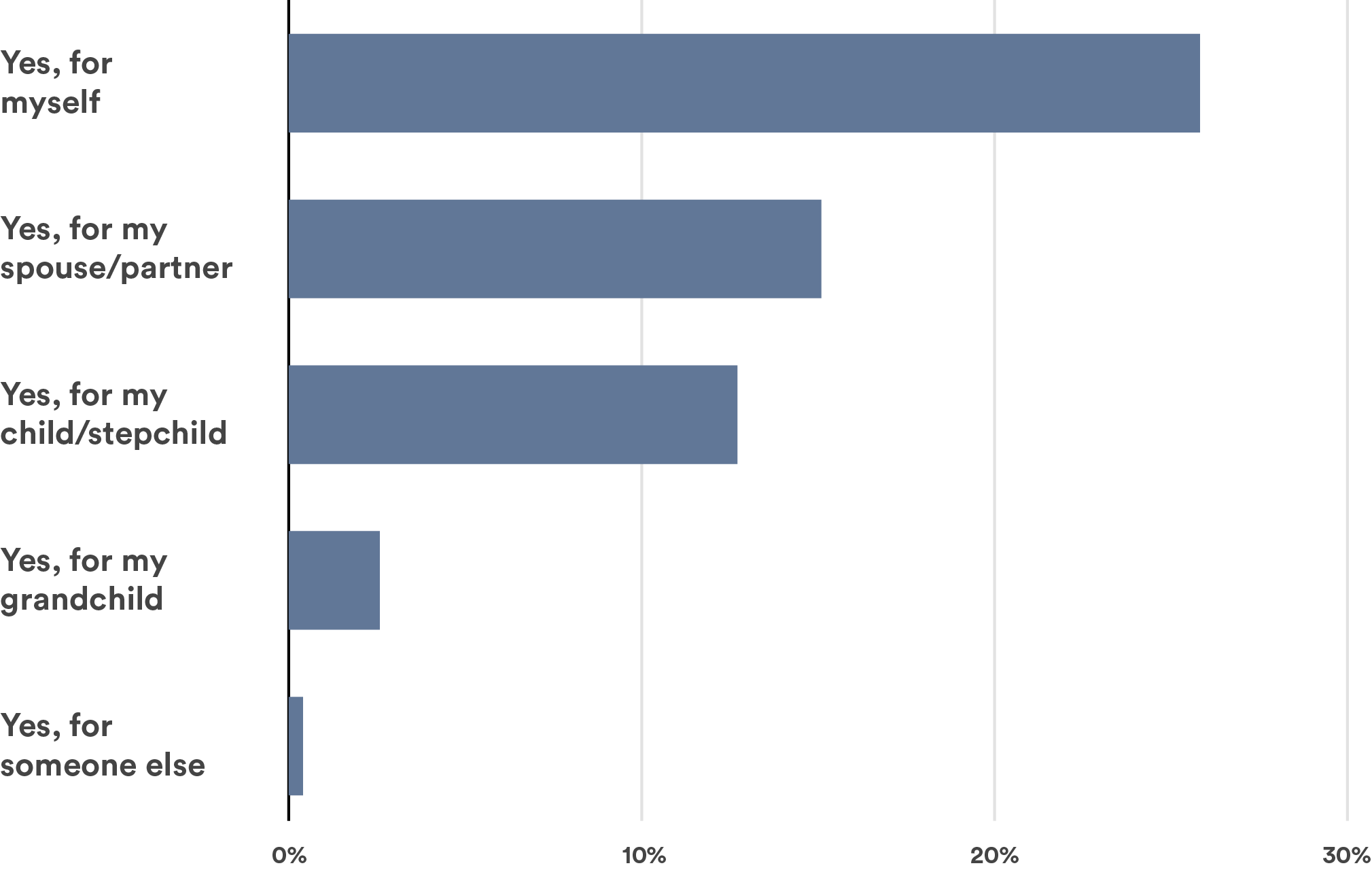

Over the past two decades, student loan balances have ballooned, growing from $260 billion in 2004 to $1.6 trillion by 2025. According to a recent Point survey, two in five (42%) American homeowners are currently paying student debt for themselves or a family member, and 37% plan to take on student debt in the future – including 10% who don’t currently have any student debt.

Do you currently have any student/education debt you are paying for?

(select all that apply)

With the typical student loan payment currently at around $500 per month – or almost a quarter of what the typical home buyer pays monthly on their mortgage – seven-in-10 homeowners with student loan debt say that it impacts their household finances by a “moderate” or “significant” amount. Among homeowners with student debt aged 55-plus, eight-in-10 say that it impacts their household finances by a “moderate” or “significant” amount. More recently, delinquencies on student debt have begun to surge: By 2025-Q2, more than one-in-10 student loan borrowers were delinquent, a rate that doubled to nearly one-in-five among older borrowers.

Recent changes to federal student debt rules create new urgency for many borrowers to rethink their student debt payment plans. As part of the sweeping One Big Beautiful Bill (OBBB) that Congress passed in July, older student loan programs will come to an end. They will be replaced with a new plan for future borrowers. Under this plan, Americans who take on education debt will end up repaying more of what they borrow over the life of their loans — largely because there are far fewer pathways to forgiveness. More than three-quarters (76%) of homeowners with student loan debt surveyed by Point say they are concerned that the OBBB might impact their ability to make their loan payments.

In the past, paying off student debt early with home equity rarely made financial sense – especially if it required taking on new debt. That old logic is now in flux. The combination of OBBB policy changes and new financial tools shifts that calculus. Moving forward, more Americans may find it attractive to prepay their student debt by accessing their home’s equity.

New policy changes mean that more student loan borrowers will end up paying more on their loans for a longer period of time.

The most important changes to student loan programs in the OBBB focus on income-based repayment. Over the past decade and a half, these programs have undergone several iterations and now cover five repayment plans with slightly different payment formulas, income exemptions, and principal and interest forgiveness conditions.

The OBBB consolidates these income-based student loan repayment programs into a single plan that is projected to increase monthly costs for low and high-income undergraduate borrowers, while reducing costs for middle-income undergraduate borrowers. Expected costs are projected to increase across the board for graduate school borrowers. Borrowers on the older plans who do not make any modifications to their loans (e.g., don’t take on new student debt) will be able to remain on those plans, but only the new plan will be available to borrowers moving forward.

A comprehensive independent comparison of the plans points to three key takeaways relevant to the calculus over whether or not to prepay the loans:

- The loan forgiveness horizon is extended from 20-25 years under the older plans to 30 years with the new plan, reducing the share of borrowers who will receive any amount of loan forgiveness and increasing total expected loan costs for borrowers;

- Economic hardship and unemployment deferments will be eliminated for new loans starting in July 2027, meaning that future loans will be less forgiving for borrowers during economic downturns; and

- Income exemptions for dependents are currently tied to the federal poverty threshold and adjust with inflation, but will be replaced with a flat payment credit that is not indexed to inflation and will erode over time. The result will, again, be to increase lifetime costs – particularly for higher-earning and married borrowers, and for borrowers with children.

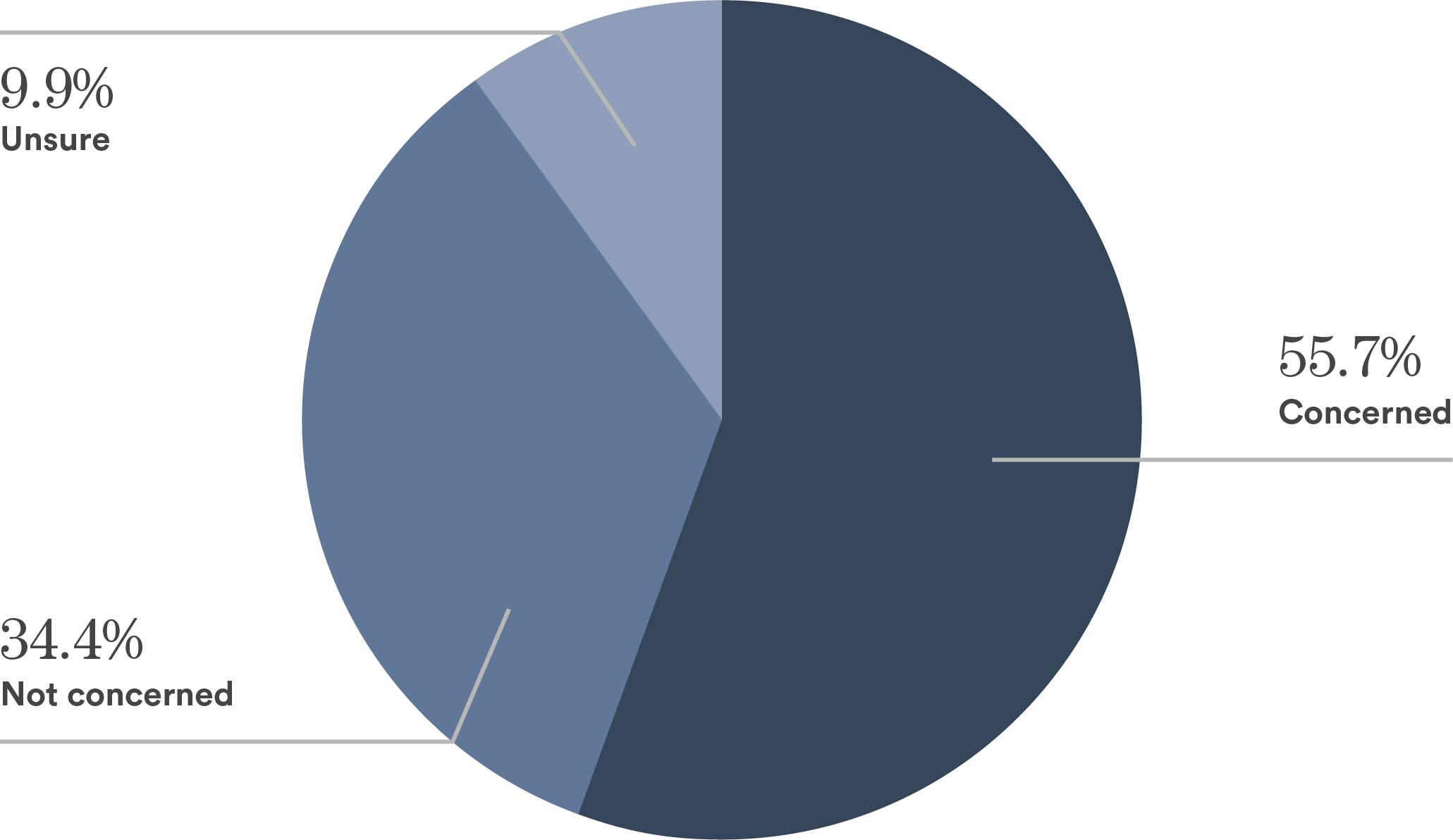

Together, these changes mean that moving forward, student loan borrowers who opt for income-based repayment plans should expect to pay more of their higher education debt over a longer period of time. Public sentiment around the bill reflects these shifts: 56% of homeowners surveyed by Point say that they are “very concerned” or “somewhat concerned” that the OBBB might impact their ability to meet current or future student loan payments.

How concerned are you about how the new federal budget bill — The One Big Beautiful Bill might impact your ability to make your current or future student loan payments?

In the past, it rarely made financial sense to pay off student debt with home equity.

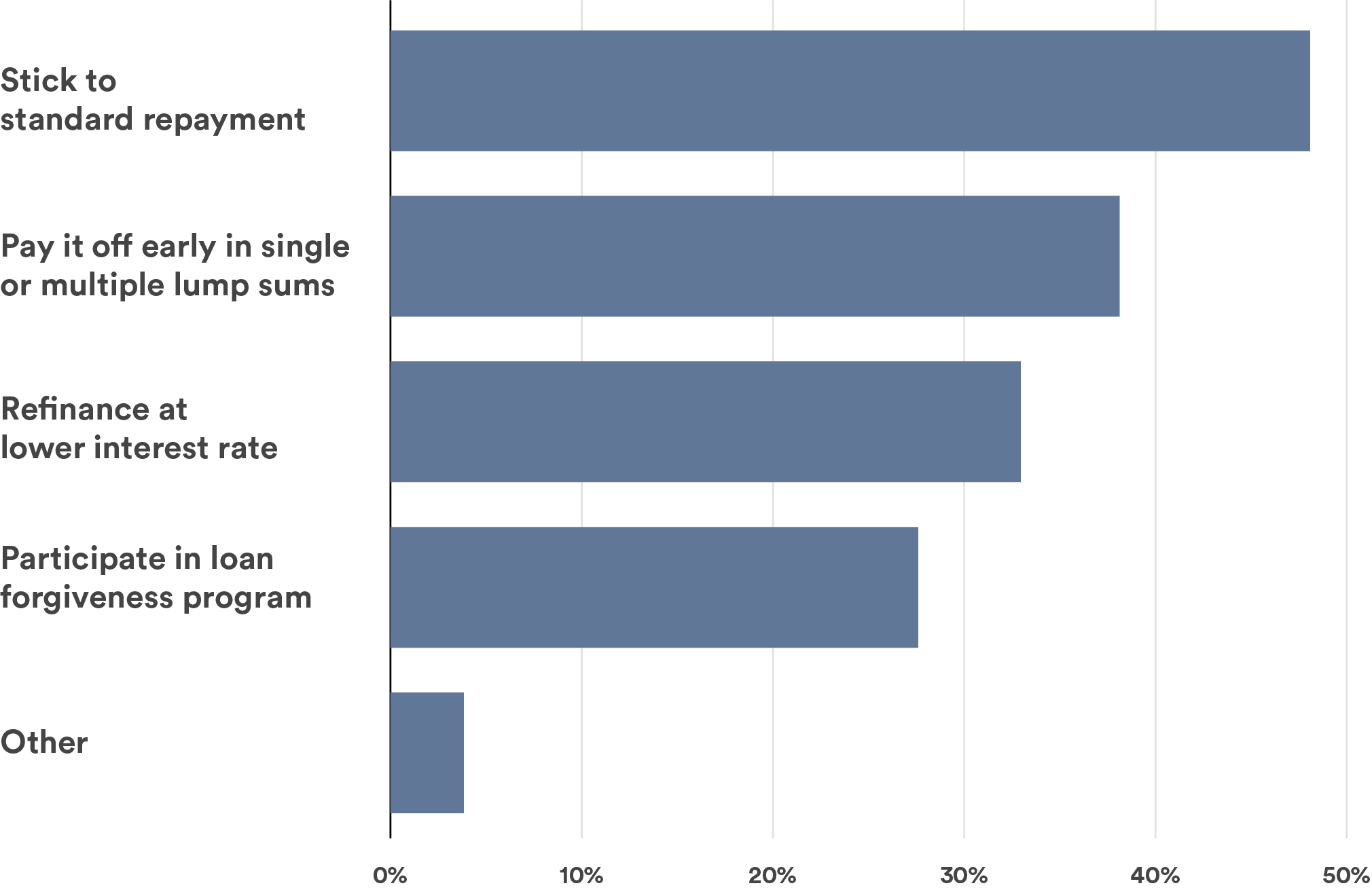

Less than half (48%) of homeowners with student debt plan to stick to the standard repayment plan, while 38% plan to repay it early. Among those who plan to stick to the standard repayment plan, 14% plan to refinance the debt at a lower rate, and 12% expect to participate in a loan forgiveness program – two options that will be substantially curtailed moving forward by the OBBB.

Which of the following best characterizes how you plan to pay any current student education debt?

About one in 10 homeowners plan to use home equity to pay off their student debt, and prepaying student debt has always provided some psychic relief for debt-averse borrowers. But in the past, it rarely made financial sense to pay off student debt balances early – especially if doing so required new financing – despite the fact that interest rates on student debt are high compared to other types of loans because:

- There have long been multiple paths to student loan forgiveness (on both interest and principal);

- There were payment deferral options in moments of need; and

- The debt was unsecured, meaning that the consequences of default were less severe than for other types of debt.

The worst-case outcome for the borrower in the case of default is wage garnishment and an adverse impact on their credit score; the worst-case outcome for a borrower on debt secured with one’s home is foreclosure.

New tools to access home equity overcome barriers that prevent student loan borrowers from prepaying education debt early in the loan, when it yields the greatest savings.

The greatest benefit from prepaying student loans occurs early on in the loan. But there have historically been two key barriers that have prevented student loan borrowers from using home equity to prepay education debt.

- First, student debt burdens prevent younger borrowers from accumulating the savings to buy homes in the first place.

- Second, there are greater savings from prepaying student debt early in the loan lifecycle when borrowers who have been able to buy a home tend to have small home equity stakes.

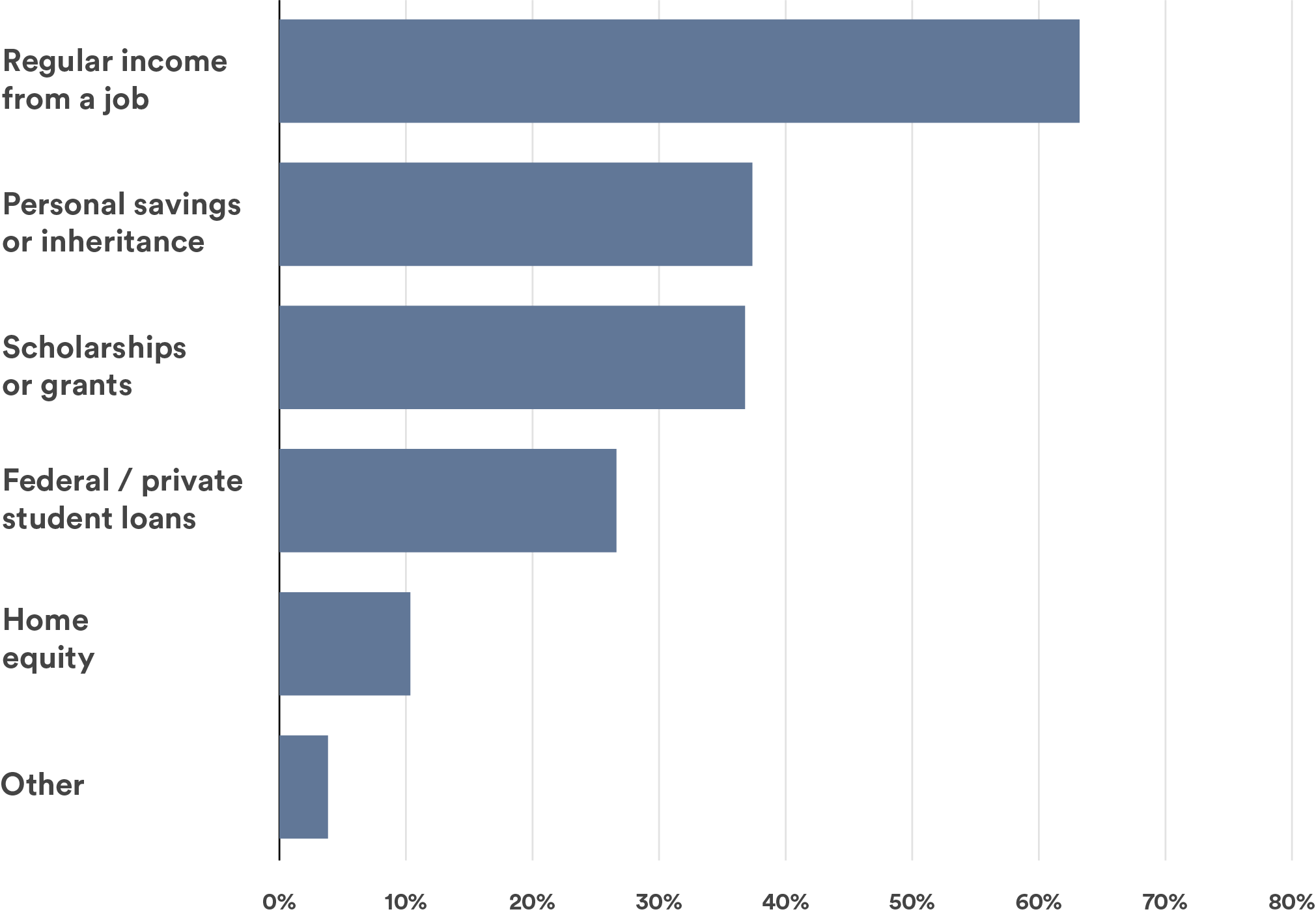

What income sources will you use to pay off current student debt or future education expenses?

The calculus differs between Home Equity Investments (HEI) and Home Equity Loans/Lines of Credit. A Home Equity Investment is a type of financing where a company gives a homeowner a lump sum of cash today in exchange for a share of the home’s future value, rather than charging monthly interest like a loan or line of credit. The HEI can be accessed at any point in a homeowner’s mortgage as long as the homeowner retains at least 2% equity in their home after the investment, and does not add to the borrower’s debt-to-income burden (so it doesn’t adversely impact credit scores).

Historically, about one in 20 (5%) of home equity investment borrowers through Point plans to use the funds to pay off education or student debt. Paying off education debt is the fifth most commonly cited use of HEI funds after debt consolidation, home renovation, buying investment properties, and investing in a business.

Conclusion

The combination of changes to student loan terms, plus new tools to access home equity, shifts the calculus on paying off education debt with home equity. In the past, student loan borrowers had a high chance of eventually having that debt forgiven. New policy changes in the OBBB mean that the pathways to student loan forgiveness will be much narrower moving forward. Paying off student debt early will become more compelling for homeowners who carry student debt, particularly if they can avoid taking on new debt through tools like Home Equity Investments.

No income? No problem. Get a home equity solution that works for more people.

Prequalify in 60 seconds with no need for perfect credit.

Show me my offer

Frequently asked questions

.png)

Thank you for subscribing!

.webp)