.webp)

Despite a fragile economy, American homeowners plan to spend more this holiday season and will put a substantial portion of it on credit cards. In a new survey commissioned by Point, most homeowners reported that they expect to carry those balances for more than one month, accruing new interest on top of already high credit card debt. Inflation, compounded by historic tariffs on consumer goods, is driving up prices across the board, making this one of the most expensive holiday seasons in recent years.

This willingness to spend, however, stands in sharp contrast to broader economic signals, such as a cooling labor market and elevated borrowing costs, suggesting a growing disconnect between the current economy and homeowners' spending.

Historically, revolving credit has helped Americans smooth spending during periods of financial strain, allowing households to maintain their lifestyles despite temporary income shocks. But today’s environment suggests those shocks may no longer be temporary. With prices still high and job growth slowing, many households could find themselves carrying elevated credit card balances for longer than they have in the past.

Most personal finance advisors recommend paying off credit card debt as soon as possible to avoid compounding interest. Homeowners with equity may be able to use home equity strategically to consolidate or pay down high-interest credit card debt and regain financial balance.

Bigger budgets and heavier borrowing define this year’s holiday outlook

Compared to 2024, more homeowners plan to spend freely this season: 44% expect their 2025 holiday spending to be higher, 17% expect it to be lower, and 39% anticipate no change. In total, the typical homeowner expects to spend between $1,000 and $1,999 on holiday-related gifts, travel, and activities this year; 6% expect to spend more than $4,000, while 24% expect to spend less than $500.

The typical homeowner plans to charge between 25% and 50% of their holiday spending to credit cards. About a quarter (26%) expect to put 75% or more of their holiday purchases on credit, and roughly one in nine (11%) say they’ll charge all of their holiday spending. High spenders rely more on credit cards: among homeowners who expect higher holiday spending this year compared to last, 57% expect to put more than half or more of that spending on a credit card, versus 33% among homeowners who expect lower holiday spending this year.

Older homeowners are driving an outsized share of holiday-related credit card spending

Older homeowners plan to put more of their holiday spending on credit cards: 11% of homeowners older than age 60 plan to put 75% or more of their holiday spending on credit cards, compared to 7% of homeowners age 45-60, and 8% of homeowners age 30-44. In general, credit card spending by older Americans – the majority of whom are homeowners – is outpacing spending by younger householders.

This year’s holiday spending will come on top of already high credit card debt loads

Credit card balances continue to climb: 54% of homeowners report carrying more debt than they did last year, and one in four (25%) say their balances are much higher. Nearly half (48%) of homeowners surveyed by Point expect their credit card debt to increase again in 2026. Total credit card debt hit $1.23 trillion in Q3 2025, up 5.7% from a year earlier and double what it was a decade ago, according to the Federal Reserve Bank of New York.

Credit card debt balance

Inflation is a big part, but not the only part, of Americans’ rising credit card debt

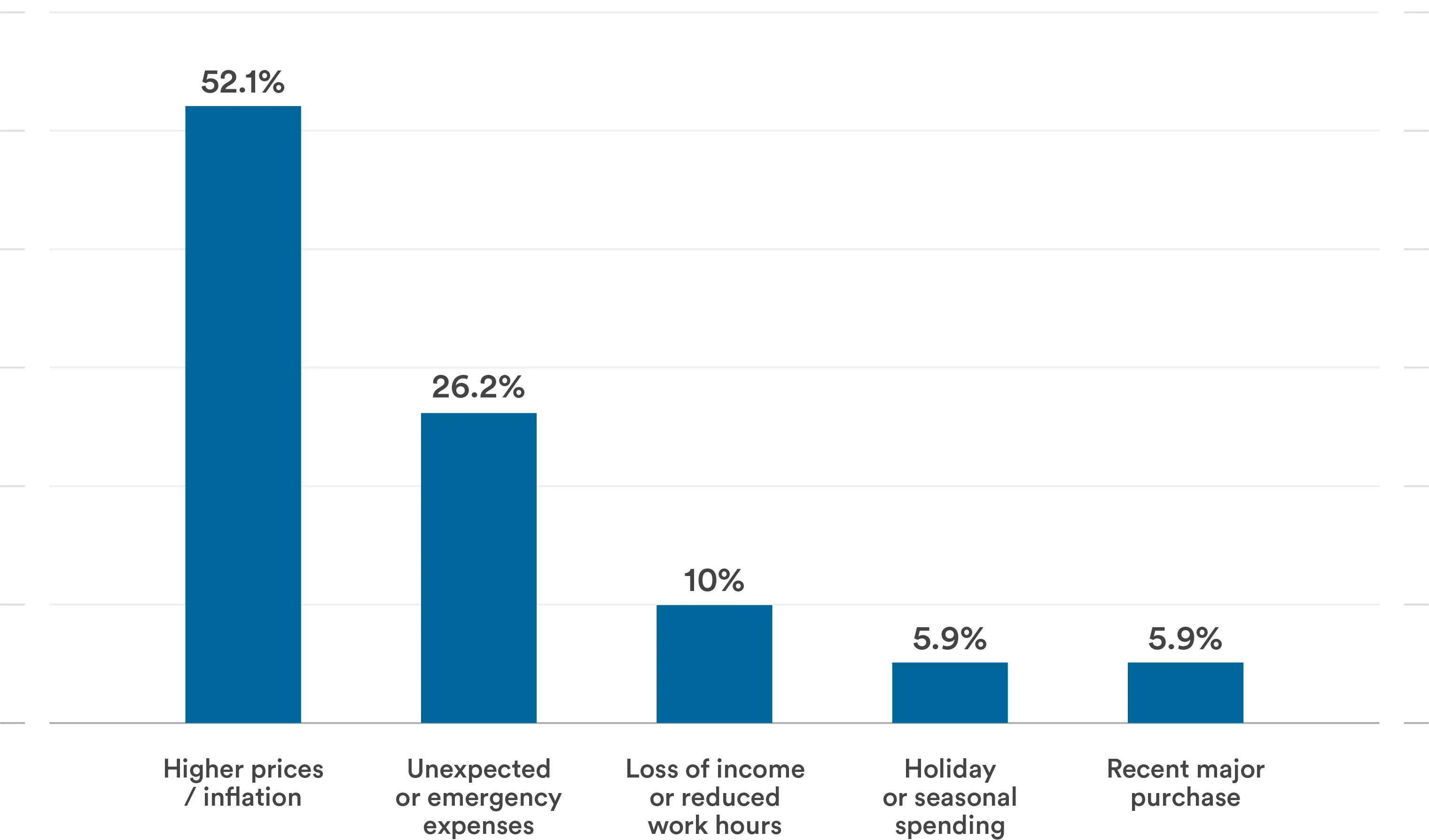

Rising prices are taking a clear toll: 52% of homeowners cite inflation as the primary reason their credit card debt has grown this year, and 56% say it’s now harder to pay down what they owe. After accounting for inflation, total credit card debt is up 2.9% from a year earlier, according to the New York Fed, while the number of credit card accounts grew even faster, by 7% year-over-year. The average inflation-adjusted balance per account hit $1,920, down from $1,998 in Q3 2024 – meaning Americans are carrying more credit cards and more credit card debt, but with less debt per card.

What’s the main reason your credit card balance has increased?

Broader economic headwinds are also contributing to the high level of credit card debt. About one in four homeowners (26%) cited unexpected expenses — such as medical or auto repair bills — as the main reason for carrying higher credit card debt, while 10% pointed to a loss of income or reduced work hours. Previous Point research showed how economic shocks, such as layoffs, can contribute to the erosion of personal finances.

Carried balances and costly rates turn holiday spending into long-term debt

Less than a third (31%) of homeowners say that they plan to pay off any holiday spending put on credit cards within a month; the remaining 69% plan to carry the credit card debt for at least a month, meaning that they will incur interest on that debt. Two in five (42%) homeowners say that they expect to carry their holiday-related credit card debt for four or more months.

While credit card terms vary substantially, typical credit card APRs – annual percentage rates, which are the annualized interest rates that apply to credit card debt carried for over a month – are currently hovering around 20%, according to Bankrate. At typical APRs, $1,500 in holiday spending would accrue about $25 in interest after one month and more than $100 after four months. For cards with higher rates, that same balance could cost nearly $40 in just one month.

Which of the following best describes how you feel about your current credit card debt?

Homeowners feeling “overwhelmed” by their current levels of credit card debt

Nearly one in four homeowners (23%) say they feel extremely overwhelmed by their current level of credit card debt, and another 17% report feeling somewhat stressed. Interestingly, holiday spending is highest among those at both extremes — those who are the most anxious and those who are the most relaxed about their debt.

Among homeowners who feel extremely overwhelmed, 63% plan to spend $1,000 or more on holiday shopping this year, compared with 47% of those who feel somewhat stressed, 39% who feel neutral or indifferent, and 56% who feel somewhat comfortable.

A similar pattern emerges in how homeowners plan to pay: 50% of those who feel extremely overwhelmed expect to put at least half of their holiday spending on credit cards, compared with 37% of those who feel somewhat stressed, 31% of those who feel neutral or indifferent, and 46% of those who feel somewhat comfortable.

More homeowners are exploring paying off credit card debt with home equity

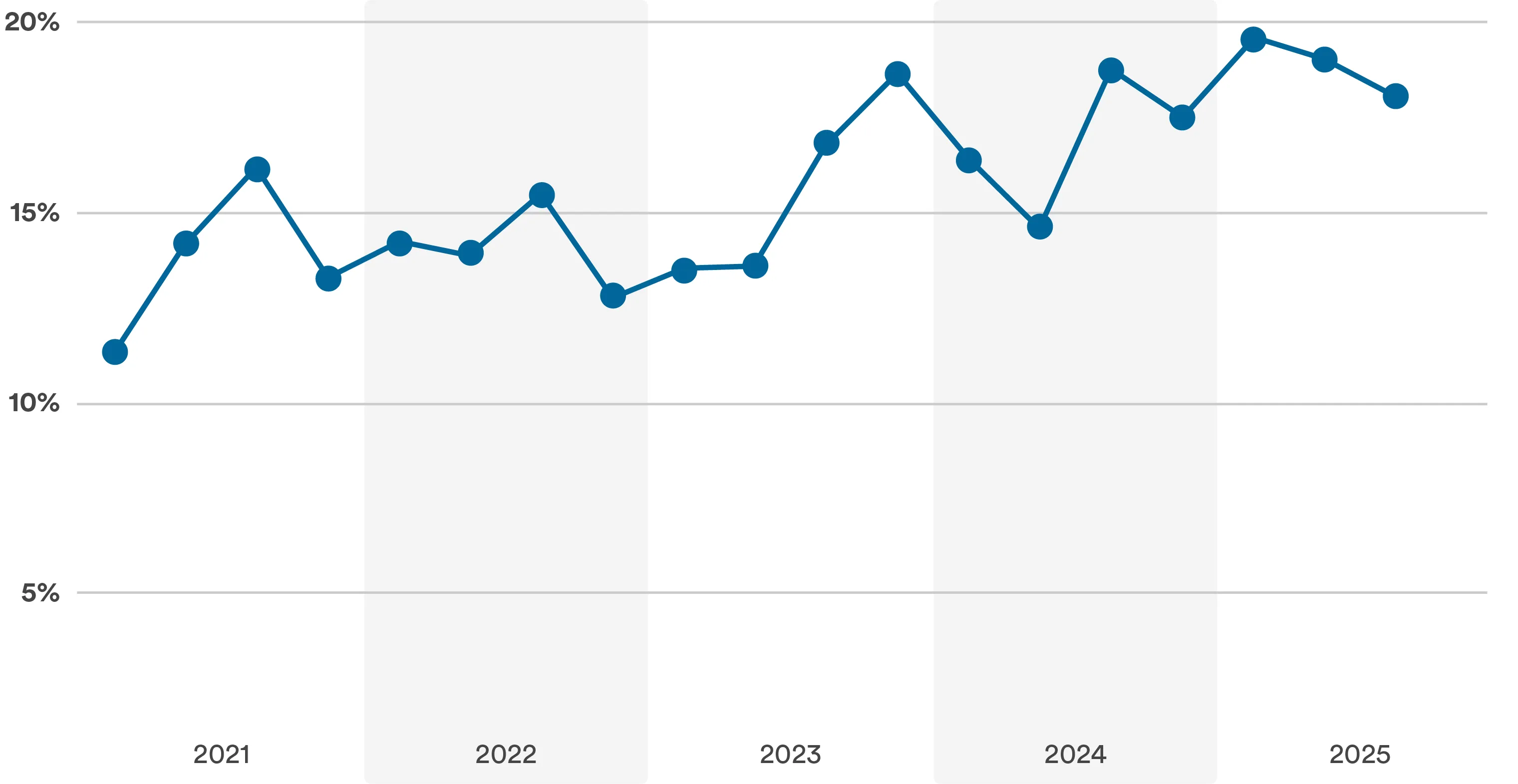

Over the past four years, Point has seen a steady increase in homeowners seeking to utilize their home equity to manage or eliminate credit card debt. In 2021, about 13% of home equity investment inquiries to Point cited credit card debt as the primary use; by 2025 (through Q3), that share had climbed to 18%, underscoring growing interest in lower-cost, equity-based solutions as credit card rates remain high.

A rising share of home equity investment inquiries cite paying off credit card debt

% of Point HEI inquiries that cite paying off credit card debt as a use for the funds.

Finding financial balance in a season of spending

The 2025 holiday season underscores the complex tradeoff facing many American homeowners: balancing optimism and tradition with rising financial pressures. Credit cards remain an easy bridge for spending, but at a time of high rates and persistent inflation, that bridge can quickly become a burden.

For homeowners, the opportunity lies in using their home equity strategically, turning a static asset into a financial tool that restores balance and resilience for the year ahead. As borrowing costs remain elevated, carrying credit card balances can quickly become an expensive proposition. For households with significant home equity, exploring lower-cost options such as home equity investments may offer a practical path to greater financial stability and peace of mind in the new year.

No income? No problem. Get a home equity solution that works for more people.

Prequalify in 60 seconds with no need for perfect credit.

Show me my offer

Frequently asked questions

.png)

Thank you for subscribing!

.webp)