.webp)

No one can predict exactly when the next recession will hit—but signs of economic uncertainty are hard to ignore. Whether it's rising interest rates, a slowing job market, or higher everyday costs, many households are feeling the pressure.

Still, it’s always a good idea to learn how to recession-proof your finances. Safeguarding your finances is all about building resilience—so you’re better prepared to weather downturns, protect your income, and stay in control no matter what the economy does next.

How to prepare for a recession

Preparing for a recession isn’t about panic—it’s about planning. From budgeting smarter to reducing debt and boosting your savings, here are several tips to help you become more financially secure:

Get a handle on budgeting

Although the thought of budgeting might seem restrictive, budgeting is really a spending plan. At the beginning of each month, review your upcoming expenses, whether it's your 6-month car insurance bill or a 6-week hair appointment.

By knowing your monthly expenses and your income, you can adjust your spending to ensure that you don't spend more than you earn. Developing this habit can help you become familiar with your spending patterns and identify areas where you can cut back if a recession hits.

Pay down high-interest debt

The average credit card interest rate is around 21% in 2025. Interest rates that high can make it challenging to get out of debt. That's because interest rates can compound and increase the amount you owe, especially if you're only able to pay the minimum each month.

If you're concerned about making payments during a recession, take the time now to aggressively pay down high-interest debt. Whether you have to work an extra job or cut down on expenses for a short time, it's worth it to pay down high-interest debt and reduce your financial responsibilities in the future.

If your credit score is in good shape, you might also consider refinancing existing loans to lock in a lower rate or consolidating high-interest credit card debt into a personal loan with more manageable terms. These strategies can lower your monthly payments and reduce the total amount of interest you pay over time.

Focus on bolstering your reserves

In addition to paying down high-interest debt, it's also a good idea to build an emergency savings account. Even having a small amount saved, whether it's with an online bank or a credit union, can help you pay for unexpected expenses.

Experts recommend keeping three to six months’ worth of expenses in a high-yield savings account. As an added bonus, when you have the funds to pay for a medical bill or a car repair, it prevents you from adding to (or falling back into) credit card debt.

Keep your credit score high

Maintaining a high credit score enables you to qualify for some of the most competitive interest rates and terms should you need to borrow money in an emergency.

A large portion of your credit score, 35%, is based on your payment history, so paying your bills on time, every time, is crucial if you want to keep a high credit score or improve the one you have. It’s also smart to keep your credit utilization low—ideally under 30% of your available credit—and to avoid opening too many new accounts at once.

A strong credit profile gives you more flexibility and peace of mind, especially during uncertain times.

Review your investment strategy

Whether you're investing now or haven't started yet, it's important to review your investing strategy. If you need help, you can always seek the support of a Certified Financial Planner (CFP) and get help reviewing your personal finances and creating a financial plan.

Ultimately, knowing your asset allocations and consulting with an advisor can help you determine how to stay the course and adjust your strategy during bear markets.

Prepare for a possible job search

If you feel that there might be job losses in your industry, it's a good idea to prepare for a potential job search. This means updating your resume, your LinkedIn profile, and reconnecting with professional contacts.

Hopefully, you won't need to apply for new jobs, but if you do, it's good to have contacts and a plan in place ahead of time.

It may also help to explore new certifications or licensures that could make you more competitive or open doors in related fields. Additionally, consider talking to your current employer about potential raise opportunities or ways to take on more responsibility—both of which can help grow your income and make you more valuable to your team. Being proactive now can ease uncertainty later.

Know your assets

When it comes to building recession-proof finances, it’s important to understand what you already have working in your favor. Your assets—things you own that have value—can play a key role in helping you weather economic downturns.

These might include your home, retirement savings, stocks, vehicles, or even valuable collectibles. Start by making a list of everything you own and estimating its current value. This will give you a clearer picture of your financial foundation and help you identify opportunities to build resilience.

For example, your home could be a source of equity you can tap into if needed, or your retirement accounts may be more diversified than you think. The better you understand your assets, the more strategic you can be about protecting and growing your wealth—even when the economy gets rocky.

Frequently asked questions

How much money do you need to be recession-proof?

There’s no one-size-fits-all number, but many financial experts recommend having at least 3 to 6 months’ worth of living expenses saved in an emergency fund to feel somewhat recession-proof. The idea is to give yourself a cushion in case of job loss, reduced income, or unexpected costs.

Beyond that, having diverse income sources, manageable debt, and investments in stable assets like real estate or bonds can add more protection. Ultimately, being recession-proof is less about hitting a specific dollar amount and more about building financial resilience.

What is the most recession-proof asset?

The most recession-proof asset is often considered to be real estate—especially residential property—because people always need a place to live, even during economic downturns. While property values can fluctuate, real estate tends to hold its value better than many other assets over the long term, and rental income can provide steady cash flow.

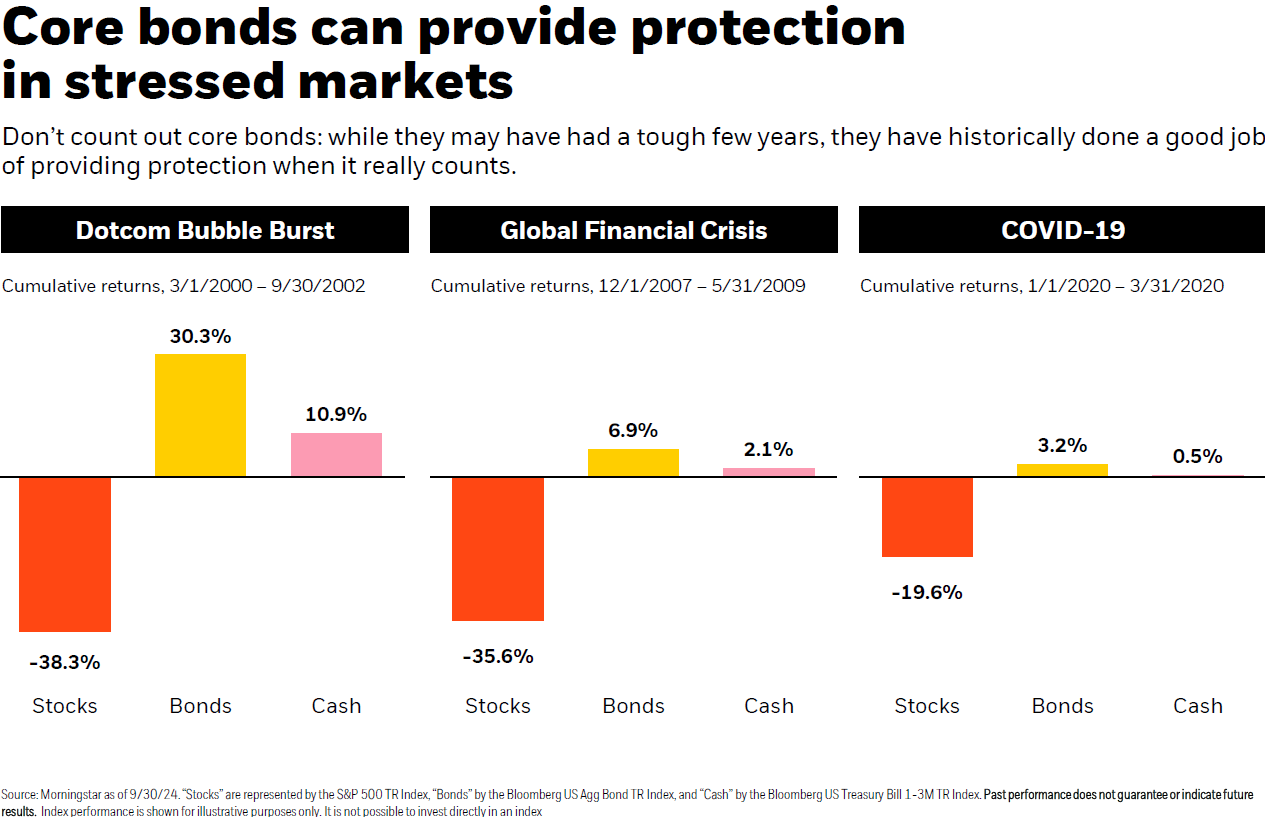

Additional data shows that during the pandemic and the 2008-2009 recession, cash and government bonds fared better than the stock market during recession years.

How to recession-proof your income?

One of the best ways to recession-proof your income is to diversify your income streams. Starting a business, having a side hustle, and exploring passive income ideas, such as investing in dividend stocks, can all help you maintain a steady cash flow in periods of economic uncertainty.

Final thoughts

Learning how to recession-proof your finances can help alleviate stress and anxiety should the economy take a downturn. The habits you establish now, like budgeting, building an emergency savings, and diversifying your income, can help you continue to pay your bills and meet your basic needs, even in the event of an economic downturn.

If you’re a homeowner looking to improve your cash flow or pay down high-interest debt, learn more about a Home Equity Investment from Point.

No income? No problem. Get a home equity solution that works for more people.

Prequalify in 60 seconds with no need for perfect credit.

Show me my offer

Frequently asked questions

.png)

Thank you for subscribing!

.webp)

{kind=link}