.webp)

Home equity has long been America’s piggy bank. The new economic reality changes that.

Each year, about 1 in 11 homeowners with a mortgage experience a labor market shock – like a job loss, a pay decrease, or becoming self-employed – events that can lead to a decline in their credit score and/or income. This can make it difficult, and sometimes impossible, to access their home equity via traditional loans exactly when they need it most.

For generations of Americans, the home has been both a safe haven and a safety net. In life’s periodic moments of economic need, home equity was usually there – to finance home renovations, to pay off high-interest debt, to fund higher education or business ventures, and in the twilight of our lives, to cover the costs of assisted living or palliative care. Steadily rising home values – fueled by the joint tailwinds of progressively falling interest rates and population growth – made home equity loans and lines of credit a natural choice for life’s periodic liquidity needs.

However, two major shifts in the post-pandemic American economy change the historic calculus.

- Higher-for-longer long-term interest rates; and

- The normalization of “jungle gym” careers and the prevalence of gig/fractional work.

“Higher-for-longer” interest rates

First, persistently high interest rates mean that tools commonly used to borrow against accumulated home equity in the past now substantially increase the borrower’s monthly debt service costs. This implies that the out-of-pocket and opportunity costs of borrowing against accumulated home equity will be higher than those of borrowing against future home equity gains.

30-year fixed mortgage rate over time

In a low-interest rate environment, a cash-out refinance can reduce a borrower’s monthly payment given substantial historical asset appreciation, but in a high-interest rate environment, the opposite happens: cash-out refis can substantially increase a homeowner’s monthly mortgage payment.

Consider the following scenario: Assume a homeowner bought a median U.S. home (priced at $230,330) in December 2018 with a 20% down payment and a 30-year fixed mortgage rate prevailing at the time (4.6%). Six years later, in December 2024, life circumstances have changed, and the homeowner decides to access $50,000 in cash. The home has appreciated in line with national trends (around 9% per year over the six years).

- In a low-interest rate environment, with 30-year fixed mortgage rates around 3.88% (roughly what prevailed in the mid-2010s), a cash-out refi would save the homeowner around $53 per month on their monthly payment (-6%).

- In a high-interest rate environment, with 30-year fixed mortgage rates around 6.76% (roughly what prevailed in 2023-24), a cash-out refi would increase the homeowner’s monthly payment by about $206 (+22%),

“Jungle gym” careers

Second, “jungle gym” careers – the idea that career and earnings trajectories are no longer monotonically upward progressions but involve periodic steps sideways or downwards – and gig/fractional work have become more common. Sideways and downward career transitions, as well as self-employment, are all associated with negative shocks to borrowers’ credit scores and the ability to document income for new/renewed mortgage debt – especially when the labor market shift is prolonged and contributes to greater debt utilization. Consumer credit scores declined for about two years following the financial market crash in September 2008, which sparked the Great Recession, and an estimated 30 million people lost their jobs. Increased debt utilization and decreased credit scores could work against homeowners trying to access their home equity precisely when they need it most.

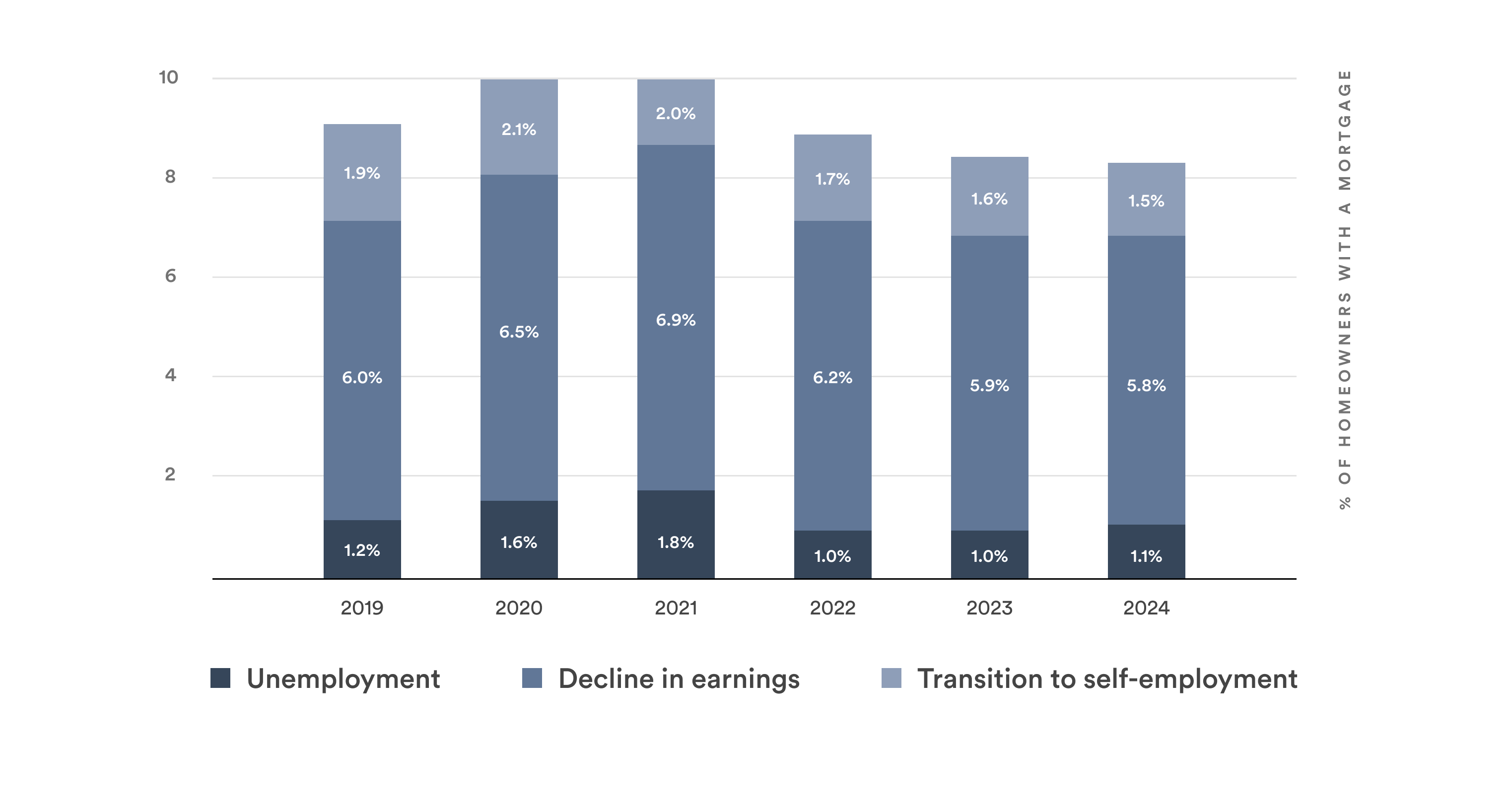

In a typical year, about 1.5% of homeowners with a mortgage become unemployed, 6.4% experience a decline in their earnings, and 1.9% become self-employed. In total, about 9% of homeowners with a mortgage experience unemployment, an income loss, or a transition into self-employment – all of which imply a negative shock to the borrower’s credit score – in a given year. In a tight labor market year like 2022-23, only 7.7% of homeowners with a mortgage experience a likely adverse credit shock, compared to 9.7% of homeowners with a mortgage in a more disruptive year like 2020-21.

Economic challenges faced by homeowners with a mortgage

published by the University of Minnesota, IPUMS-CPS.

Among those with a mortgage, non-white homeowners (9.9% versus 8.8% for white), men (9.5% versus 8.4% for women), and middle-aged homeowners (table below) were slightly more likely to experience a labor market transition associated with a negative credit shock.

Homeowners who’ve experienced

labor market transition associated

with a negative credit

shock in a typical year

In total, among the roughly 52 million homeowners with a mortgage, we estimate that 4.6 million experience a labor market shift usually associated with a negative credit score shock over a given year. Given a median nationwide home value of $356,585 (as of December 2024) and an estimated mean loan-to-value ratio of 0.44 for existing mortgage holders, that translates into about $731 billion in “locked-in” home equity due to plausible credit score shocks associated with work transitions.

The share of homeowners with a mortgage who likely experienced an adverse credit shock is very similar across regions of the country. However, there are slight differences: 8.9% in the Northeast, 9.0% in the South, 9.1% in the Midwest, and 8.9% in the West. By region, that amounts to a total “locked in” home equity of $149 billion in the Northeast, $247 billion in the South, $121 billion in the Midwest, and $284 billion in the West.

Official employment data through the first two months of 2025 do not fully capture recent dislocations in the U.S. labor market — including major private-sector and public-sector layoffs. It is expected that in 2025, more and more American homeowners will face the conundrum of needing to access liquidity amid a negative shock to their employment, income, and credit.

Conclusion

Life moves quickly, and circumstances change — often unexpectedly — after home purchases: jobs, families (divorce, eldercare), disabilities, etc. A generation of homebuyers who locked in interest rates between 2010 and 2021 now faces a conundrum: after rapid appreciation over the past few years, their accumulated home equity is a substantial source of personal wealth, but high interest rates make it either impossible or prohibitively costly to access that wealth.

The simple old solution of selling your home to trade up or down isn’t always realistic. Borrowing against home equity isn’t an option for many American homeowners either. According to Home Mortgage Disclosure Act data, HELOC denial rates remain steadily above denial rates for conventional mortgages.

The economy and careers have changed since banks first began supporting homeowners in accessing their accumulated housing wealth. However, the ways we access that wealth have not kept pace with changes in the economy. Home equity lending is increasingly a solution for an age-old challenge amid new economic realities.

Methodology

Estimating the number and share of homeowners with a mortgage who have likely experienced an adverse credit score shock over the previous year.

- No public data set includes information on both (a) mortgage borrowing status, and (b) annual changes in employment or income. The U.S. Census Bureau’s American Community Survey (ACS) contains (a) but not (b), while the longitudinal Current Population Survey (CPS) contains (b) but not (a).

- To overcome this limitation, we built a predictive model of mortgage status using ACS data and imputed mortgage status predictions onto the CPS.

- The model used is a probabilistic (logit) Lasso, a machine learning model which takes a range of demographic variables included in both data sets – including but not limited to age, income, race/ethnicity, employment and marital status (and transformations thereof) – and estimates the most powerful predictors automatically dropping the variables with little predictive value.

- The model is cross-validated on a holdout 10% sample of the data, and then used to impute mortgage status on the CPS data.

- Using the CPS data, we then identify homeowners with a mortgage who have experienced a job loss, a decline in weekly earnings, or a shift into self employment over the previous 12 months. The results are presented in aggregate, and by race/ethnicity and age.

Estimating average home equity. Using 2023 American Community Survey (ACS) data, we estimate the distribution of tenure duration (i.e., when they moved into their home) for householders with a mortgage. Following a standard exponential amortization schedule assuming a loan-to-value ratio (LTV) of 0.8 in year 1 of the mortgage, and 0.1 in year 30 of the mortgage, we impute assumed LTVs for each point in the ACS tenure distribution and compute a weighted mean LTV. (We do not assume that LTV converges to zero in year 30 of the mortgage to allow some scope for refinances and home equity borrowing.) Home values used in the calculation correspond to Zillow’s published national median home value.

Appendix 1:

Demographic Detail on “Locked-in” Homeowners

with a Mortgage

Appendix 2:

The “Happy Valley”

Individuals who have purchased a home very recently quite naturally expect it to be difficult for them to obtain new credit over the next 12 months. After about three years, they tend to experience a sharp improvement in their confidence about their access to credit. Beyond five years, however, that sense of security begins to erode. Naturally, life circumstances change, and homeowners with longer tenures beyond five years are only slightly less confident in their ability to access credit than homeowners who purchased in the past two years, according to data from the Federal Reserve Bank of New York’s Survey of Consumer Expectations.

No income? No problem. Get a home equity solution that works for more people.

Prequalify in 60 seconds with no need for perfect credit.

Show me my offer

Frequently asked questions

Thank you for subscribing!

.webp)