.webp)

Key Takeaways

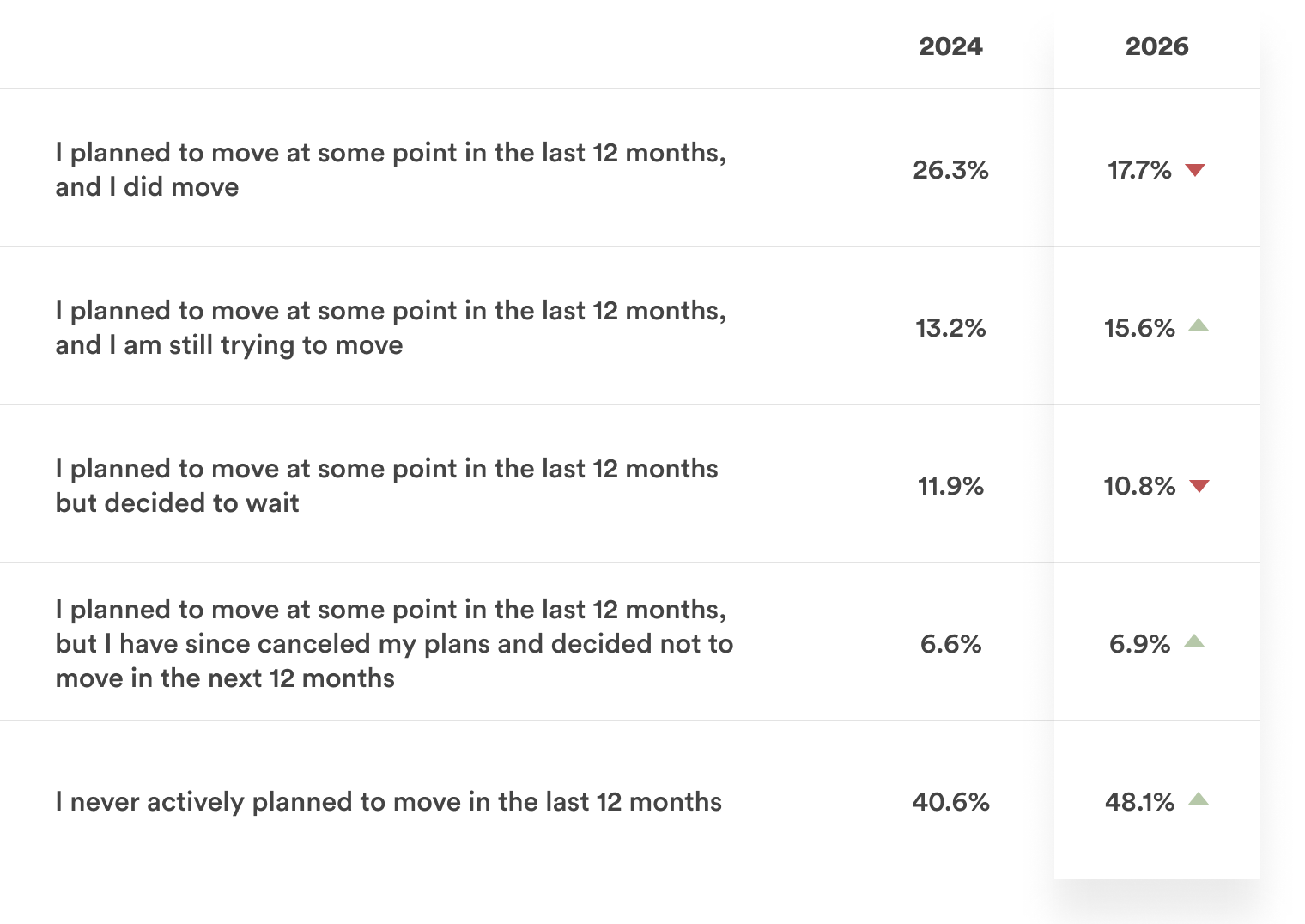

- Nearly half (48.1%) of homeowners did not even consider a move in the past year, an increase from 40.6% in 2024.

- Mortgage rates are deterring fewer movers: Among homeowners currently wanting to move, but who say they’re unlikely to do so in their desired time frame, 44.9% cited high mortgage rates as a factor – down from 55.4% in 2024.

- More people are canceling moving plans because of life factors: Around 3 in 10 (29.2%) of those who canceled plans to purchase a home did so due to a change in life circumstances (like a job or family situation) – nearly double the share who said the same in 2024 (15.9%).

- Around two-thirds (65.3%) of homeowners are planning home renovations in the next 12–18 months – a similar share compared to 2024.

- About a third (33%) of the homeowners planning to finance a renovation say today's rates make cash-out refinances and HELOCs inaccessible. This number has only dropped around 2 percentage points from 2024, despite rate cuts, indicating that the equity access gap remains an issue.

More homeowners say they are staying put due to life factors. According to the latest research by Point, fewer homeowners have considered a move in the past 12 months than in 2024. Changing life circumstances have homeowners canceling their plans to sell for reasons beyond mortgage rates and home prices.

As a result, the housing market is increasingly experiencing a structural freeze. Barriers to buying a home are expanding from macroeconomic to personal circumstances. Homeowners are responding by investing in the homes they're staying in, and by tapping the equity they've built.

The market has not thawed

During and immediately following the pandemic years, the housing market was in a frenzy marked by low rates, surging prices, and intense competition. But as interest rates rose starting in 2022, the market slowed.

By 2024, a deep freeze had set over the housing market, with 40.6% of surveyed homeowners saying they never considered a move in the prior 12 months, according to Point data. In 2026, that figure has risen further, to 48.1% — an increase of nearly 8 percentage points.

Did you actively plan to buy a home at any point in the last 12 months? If so, did you end up moving?

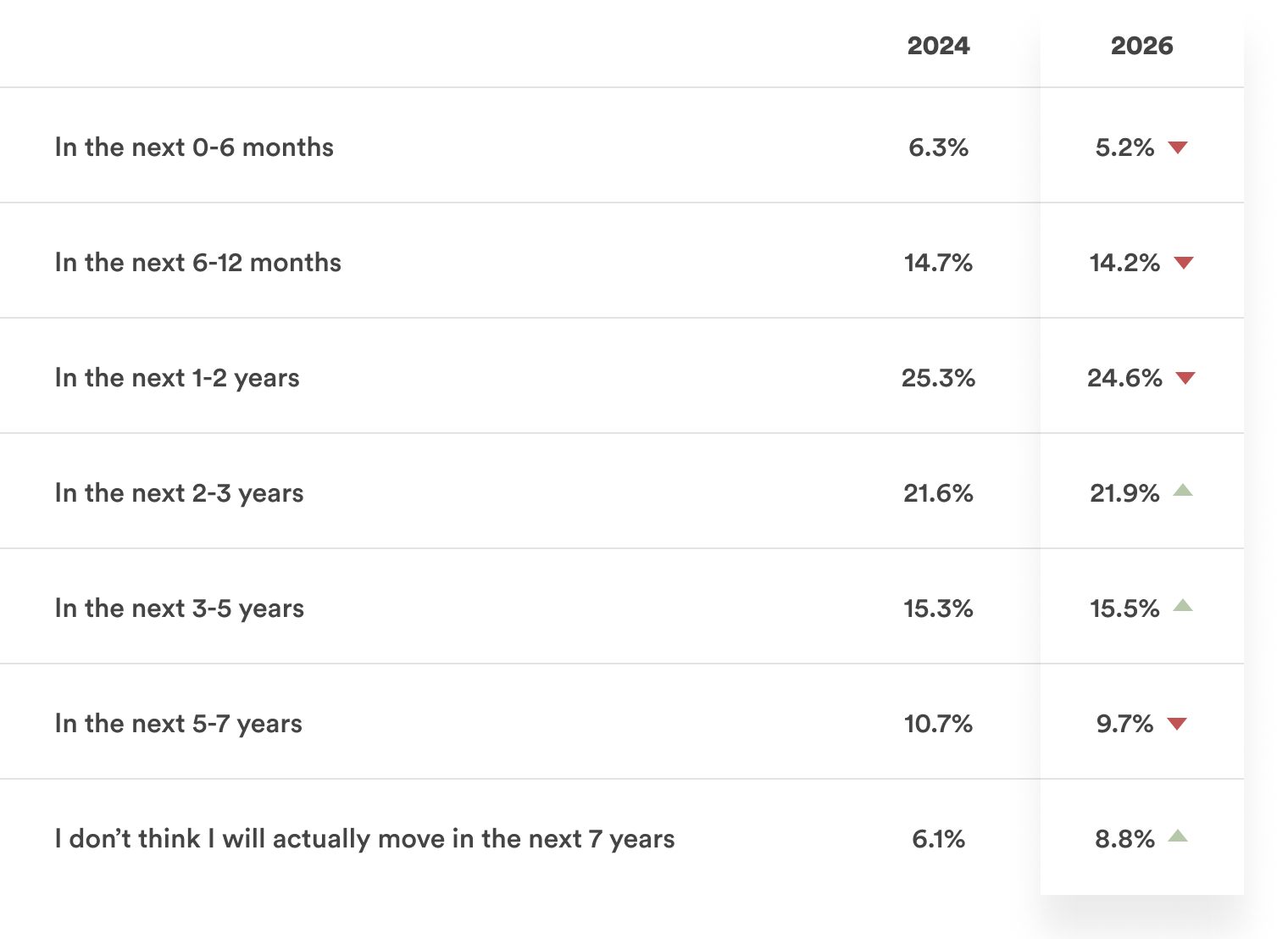

Among the 51.9% of homeowners who want to move, the gap between aspiration and expectation has grown. Only 5.2% of homeowners who want to move believe it will actually happen in the next six months, down from 6.3% in 2024. Around 8.8% say they don't think they'll move within the next seven years, up from 6.1% who said the same in 2024. The divide is gradually widening between the goal and the practical realities.

When do you think you will actually move, if at all?

New forces beyond the market are strengthening the freeze

Point’s 2024 report captured a housing market paralyzed by interest rate shock. The 2026 data reveals the compounding factor of labor market disruption.

Job instability is undermining housing plans for a meaningful share of American households, even as headline unemployment figures have appeared manageable. According to the U.S. Census Bureau's Current Population Survey, 3.6% of households had a member who experienced a layoff in the 12 months ending March 2026, while 7.3% had a member who was unemployed during that period

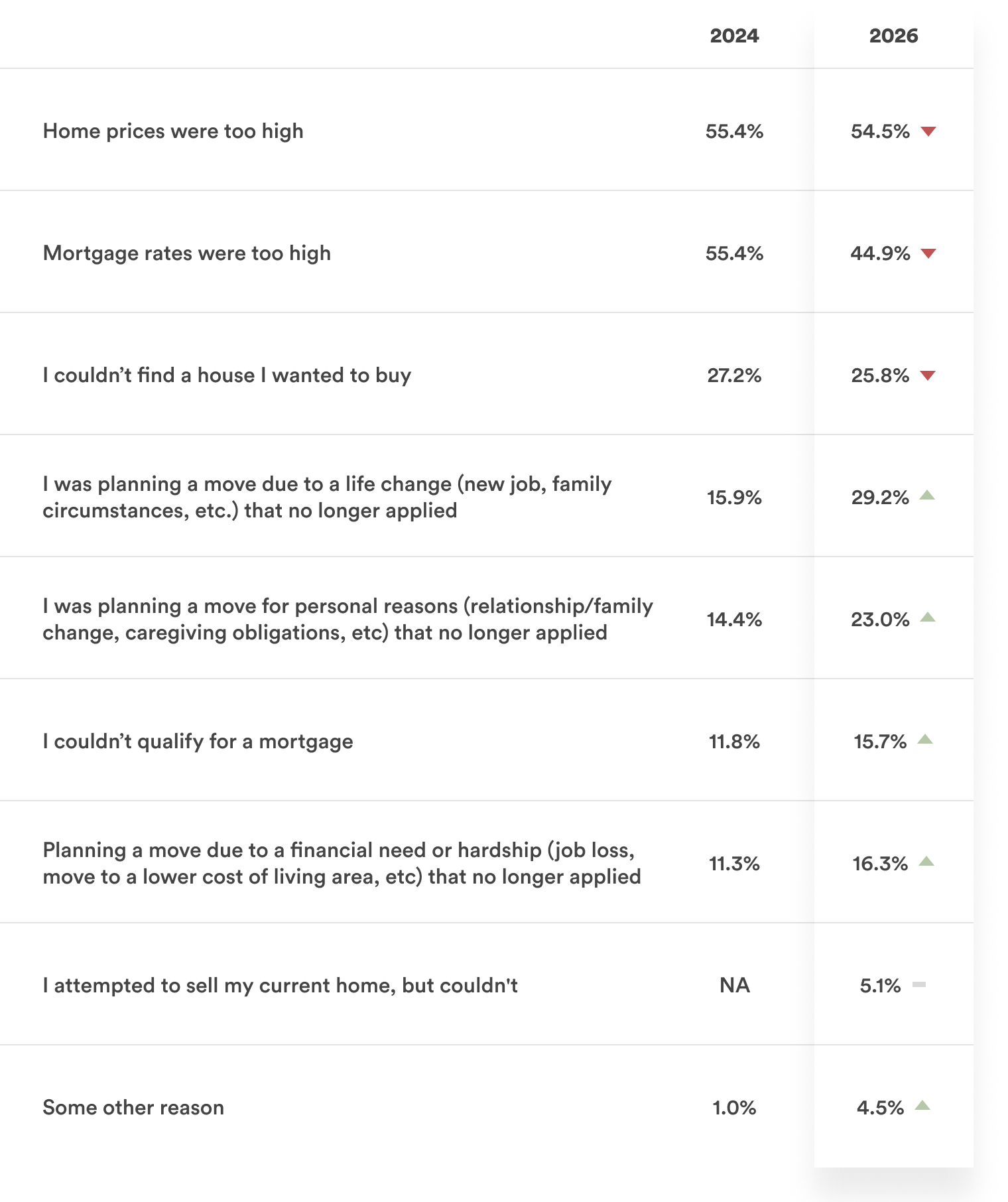

Among homeowners who canceled moving plans entirely, 29.2% cited changed life circumstances as the reason, which is nearly double the amount of people who said the same in 2024 (15.9%). In 2026, 16.3% of homeowners who canceled their plans to move said they had been planning to move due to a financial need or hardship that no longer applied, and 23.0% cited personal reasons such as relationship changes and evolving caregiving obligations as the reason for canceling their plans.

Why did you decide to delay or cancel your plans to move? Select all that apply.

Taken together, these "life happened" reasons now rival market-based barriers as explanations for canceled moves. The story of housing gridlock in 2026 is no longer just about the lock-in effect of low-rate mortgages or the sticker shock of elevated home prices. It's about a population of homeowners whose personal and financial circumstances have been destabilized — and who, facing uncertainty at home and at work, have chosen to stay put.

Home prices remained the single most-cited barrier to moving at 54.5%. Mortgage rates as a stated barrier, however, fell to 44.9% in 2026 (from 55.4% in 2024), showing a meaningful drop that reflects, in part, some easing in rates over the intervening period. But the fact that rate sensitivity is declining while overall mobility is also declining tells a nuanced story, as the market isn't unlocking as rate anxiety recedes. Life disruptions, deepened by an abundance of caution, have stepped in to keep the market frozen.

What it would take to move

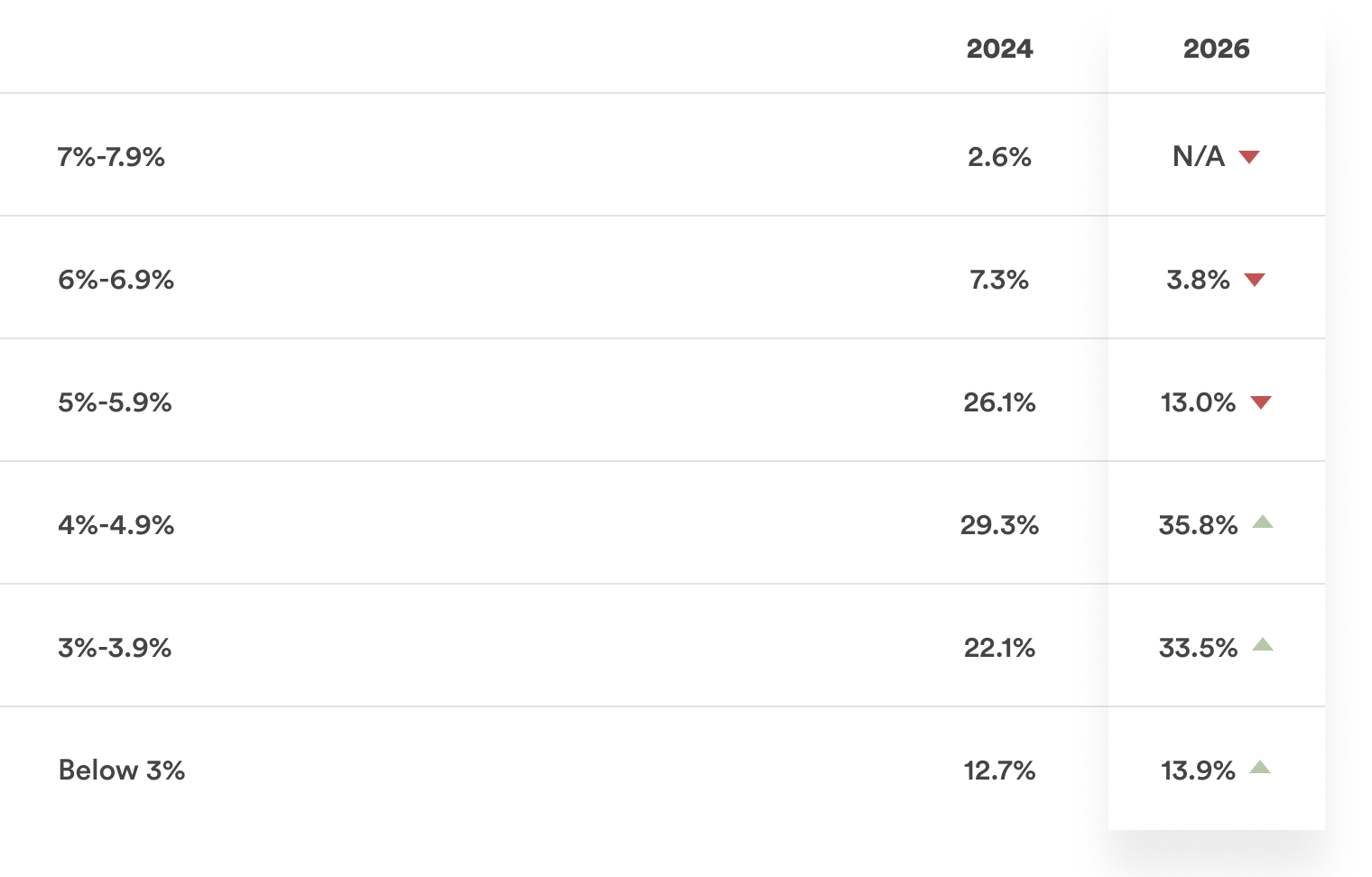

For homeowners who do want to move but feel stuck, the threshold for action remains daunting and has actually shifted higher over the past two years. Over a third of aspiring movers in 2026 (35.8%) say they'd need mortgage rates between 4% and 4.9% in order to consider a move, and nearly half (47.4%) said they'd need rates below 4%.

What would mortgage rates need to be for you to consider purchasing another home in the next 6-12 months?

These expectations reflect not just rate sensitivity but a broader recalibration of what "affordable" feels like. A generation of homeowners locked in rates between 2.5% and 3.5%, and now has internalized those numbers as the baseline, making anything above 5% feel unacceptable. This expectation gap has widened over time, not narrowed. Even as market rates have dipped modestly from peak levels, homeowners' required thresholds have moved in the opposite direction.

The lock-in effect is explicit in the data: 43.6% of would-be movers say that mortgage rates higher than their current rate would stop them from moving in their desired timeframe, and 51.6% cite home prices that remain too high. Inventory constraints persist as well, with 21.7% of respondents citing a lack of homes to choose from.

What would stop you from moving in your desired timeframe? Select all that apply.

The primary reasons homeowners want to move have also shifted subtly. Upsizing remains the top driver at 27.7%, up from 24.9% in 2024. The desire to relocate outside one's current metro area held roughly steady at 14.1%. And down from 11.1% in 2024, 7.8% cite accessing their home equity as the primary reason they'd want to move, a figure that, despite the decline, reflects a cohort of homeowners who view a sale as fundamentally a liquidity event, not just a lifestyle change.

Staying put, but not standing still

If homeowners can't — or won't — move, they aren't necessarily waiting passively. Among those who have decided not to move, nearly half (48.7%) say they will renovate their current home instead, and nearly two-thirds (65.3%) of all homeowners plan to perform renovations in the next 12 to 18 months.

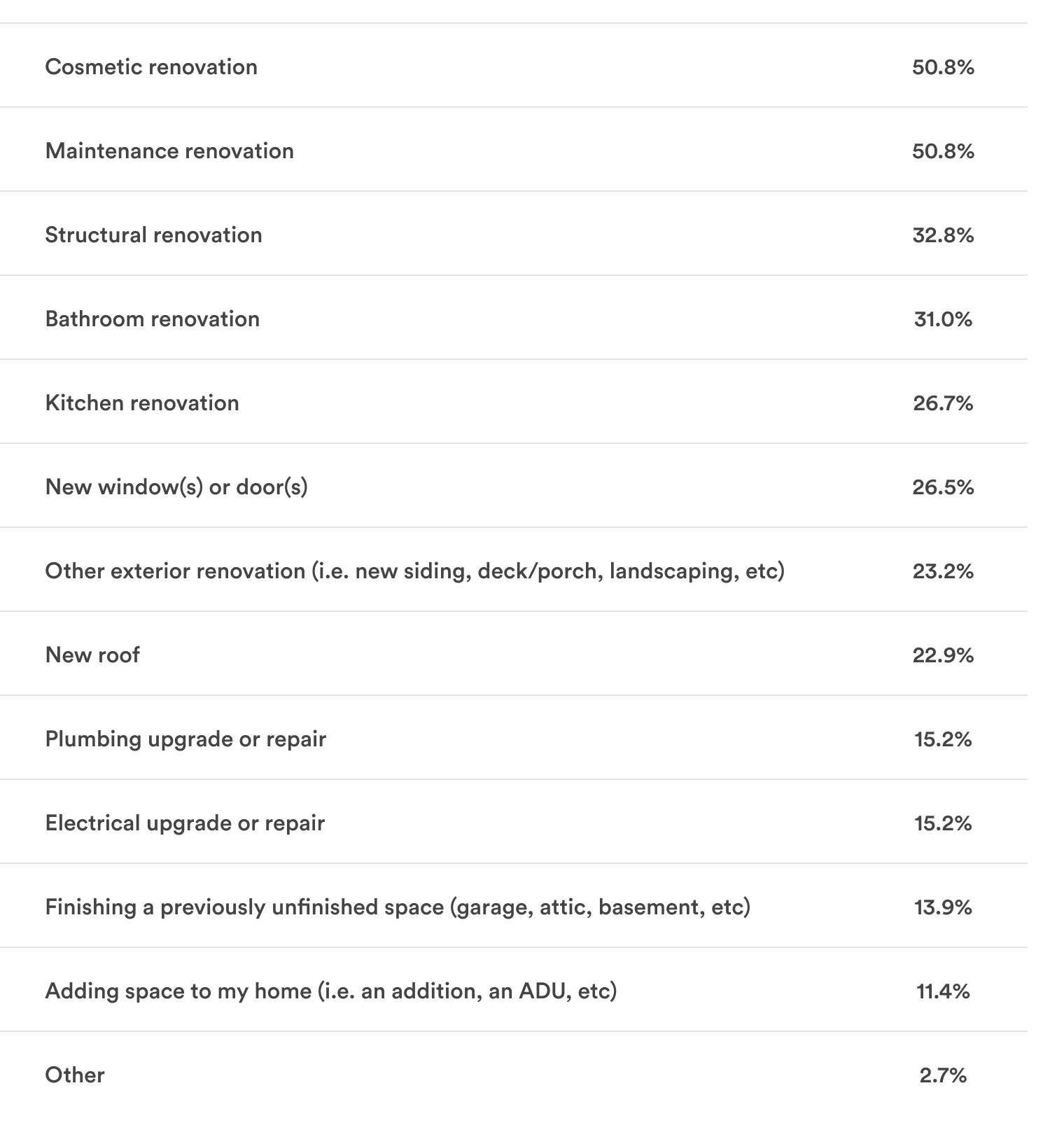

The scope of planned projects is substantial. The most common renovations are cosmetic (50.8%) and maintenance-related (50.8%), while others are pursuing kitchen renovations (26.7%), bathroom renovations (31.0%), and structural work (32.8%). About a quarter (25.1%) of homeowners planning renovations are adding space to their home, be it an addition, an ADU, or finishing a previously unfinished area, suggesting that some are expanding in place rather than trading up.

What kind of renovations are you planning? Select all that apply.

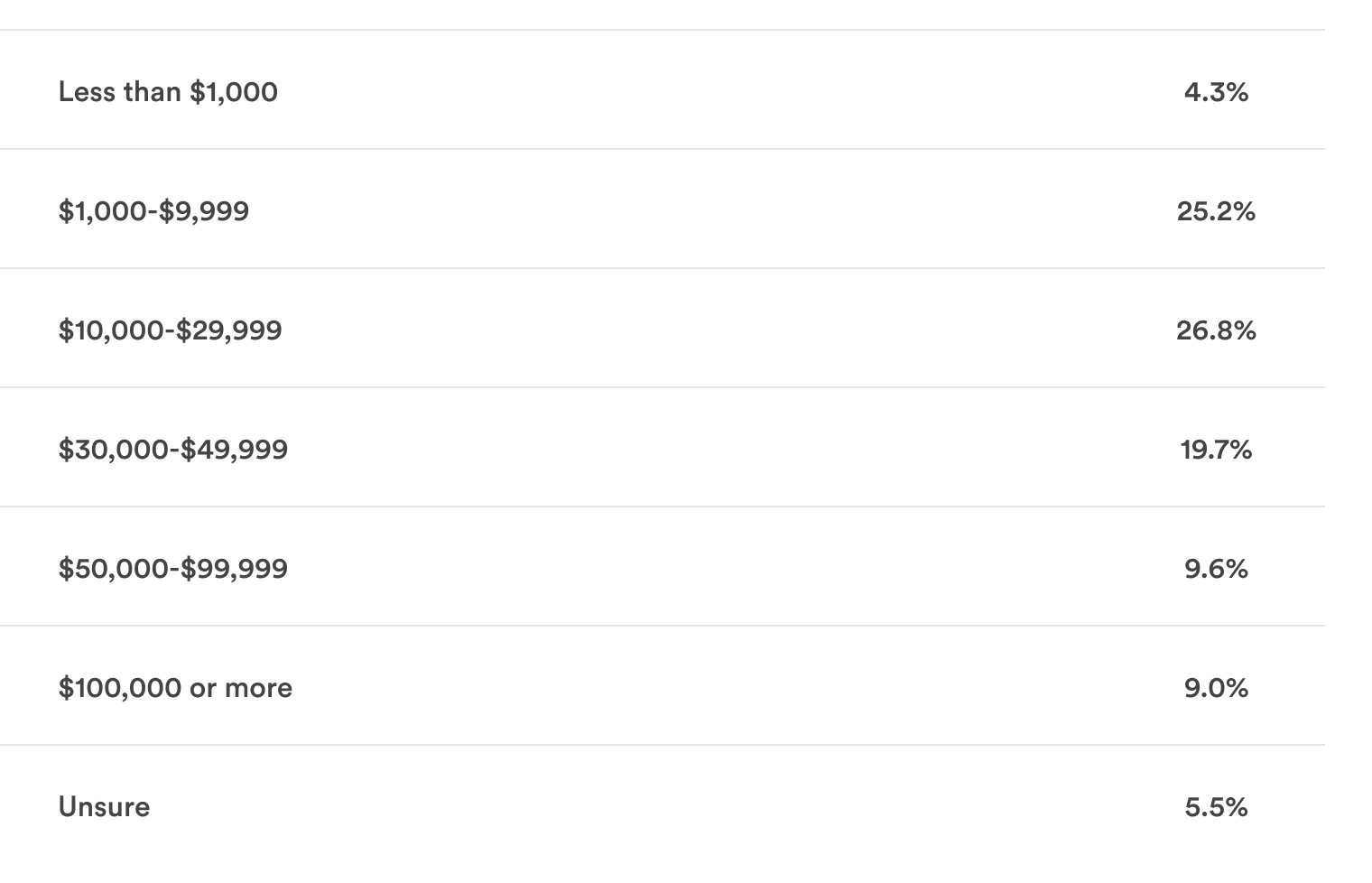

As for budgets, 19.7% of renovation planners are budgeting between $30,000 and $49,999, 9.6% are budgeting $50,000–$99,999, and 9.0% are planning to spend $100,000 or more. Combined, more than a third of renovation-planning homeowners are committing $30,000 or more to their projects, reflecting significant investment in the property, not just casual upkeep.

What is your budget for home renovations?

Homeowners are adapting their homes to their needs by creating aging-in-place features, expanding for multigenerational households, and updating kitchens and baths for the long stay. Essentially, they are making their homes work.

The equity access gap

All of this renovation activity raises a fundamental question: how are homeowners paying for it? The most common answer is cash, cited by 38.4% of those planning renovations, consistent with 38.9% in 2024 – but also means that roughly six in ten homeowners need financing for their planned renovations.

Cash-out refinances (21.1%, up from 13.5% in 2024) and HELOCs (12.7%, down from 13.8% in 2024) together account for about a third of planned financing approaches. However, these traditional home equity products come with rates that make them a non-starter for millions of homeowners under the current environment.

Among homeowners who aren't planning to use a cash-out refinance or HELOC, 32.9% will not because interest rates on those products are too high. That figure is improved from 34.7% in 2024, but the improvement is minimal given the rate movement that has occurred in the intervening period. Two years into a rate-easing cycle, approximately one in three homeowners who need equity access still can't or won't use the conventional mechanisms to get it.

The result is a persistent equity access gap. American homeowners are sitting on record levels of home equity, but year after year, the conventional bridges to that wealth remain blocked for a meaningful share of the population. This sustained inaccessibility keeps demand alive for alternative equity access products that don't require taking on new monthly debt at elevated rates, while still allowing homeowners to leverage the value of their homes.

The gap also shows up in how homeowners fill the financing void when traditional products are not an option. Credit cards are cited by 15.3% as their primary renovation financing method (17.5% in 2024) and remain a common fallback, often at significantly higher cost than a home equity product.

The portrait of a stuck homeowner

Across three years of data, a portrait emerges of the stuck American homeowner and how they're adapting.

They've been in their home for a long time: More than half (51%) have lived in their current home for more than seven years, including one in five (20.4%) who have lived in their current home for more than 20 years, per Point data. Many of these owners locked in historically low mortgage rates or have watched their home appreciate substantially, but are unable to make the math work to trade up or relocate.

They're worried about more than their mortgage rate. A greater-than-average number of their households have been impacted by layoffs in the past year, introducing a new dimension of uncertainty.

They're not passive. Nearly half of “stuck” homeowners are planning renovations. They're expanding for family needs, updating kitchens and baths, or investing in maintenance and structural improvements.

They're increasingly pessimistic about their timeline. In 2024, 6.1% of would-be movers didn't think they'd move in the next seven years. In 2026, that share rose to 8.8%.

Gridlock as a new normal

Point’s data paints a picture of a market that has reorganized itself around immobility, and of homeowners who have adapted their finances, plans, and expectations accordingly.

This freeze is no longer a temporary condition that a few rate cuts will resolve. Even as mortgage rates have eased from peak levels, homeowners' required thresholds for moving have increased. Life considerations increasingly exist wherever rate anxiety has receded.

What has remained constant across all three years of this study is homeowner investment in renovation. Homeowners can't move, but they are investing. They have equity that they can't easily access through traditional channels, but they are finding ways to use it. They have deferred the move, but not the ambition to have a better home.

That sustained investment behavior — and the equity access gap that shapes it — will define the housing economy for years to come. Homeowners are making consequential decisions that are reshaping the market in ways that extend beyond any single rate cycle.

Methodology

Point's 2026 Moving & Sentiment Study surveyed 1,007 U.S. homeowners in early 2026. The survey was nationally distributed across major U.S. regions, with respondents spanning age groups and household income levels. All respondents confirmed owner-occupancy of their primary residence. Year-over-year comparisons reference Point's 2024 Moving & Sentiment Study (n=1,076). The 2026 survey introduced new questions on household layoff experience.

No income? No problem. Get a home equity solution that works for more people.

Prequalify in 60 seconds with no need for perfect credit.

Show me my offer

Frequently asked questions

Thank you for subscribing!

.webp)